Table of Contents

- Key Features of Retirement Income Planning Software for Advisors

- Comprehensive Cash‑Flow Modeling

- Tax‑Optimized Withdrawal Strategies

- Longevity and Health‑Care Risk Modules

- Dynamic Portfolio Rebalancing

- Client‑Facing Dashboard

- Integrating Retirement Income Planning Software for Advisors into Your Practice

- Data Migration and Connectivity

- Training and Certification

- Compliance and Documentation

- Pricing Models and ROI Assessment

- Best Practices for Maximizing Client Outcomes with Retirement Income Planning Software for Advisors

- Conduct Regular Plan Reviews

- Educate Clients on Assumptions

- Leverage Scenario Planning for Risk Management

- Integrate with Broader Financial Planning

- Utilize Benchmark Comparisons

- Choosing the Right Vendor: A Checklist for Advisors

- Future Trends Shaping Retirement Income Planning Software for Advisors

- Artificial Intelligence and Predictive Analytics

- Integration of Behavioral Finance Insights

- Real‑Time Data Feeds

- Enhanced Security and Privacy Measures

- Putting It All Together: A Practical Example

Financial advisors today face an increasingly complex landscape when helping clients secure a reliable income stream for retirement. The shift from defined‑benefit pensions to defined‑contribution plans places the onus on individuals—and their advisors—to project cash flow, manage longevity risk, and adapt to market volatility. To meet these demands, many advisory firms are turning to specialized retirement income planning software for advisors, tools that combine sophisticated modeling with client‑friendly reporting.

Unlike generic financial planning platforms, retirement income planning software for advisors focuses on the post‑work phase, integrating Social Security strategies, required minimum distribution (RMD) calculations, and tax‑efficient withdrawal sequencing. By automating these intricate calculations, the software enables advisors to deliver personalized, data‑driven recommendations while maintaining compliance and scalability.

In the following sections we will examine the core functionalities that define a high‑quality solution, discuss how advisors can integrate the software into their existing workflows, and outline best practices for maximizing client outcomes. Whether you are a solo practitioner or part of a larger wealth management team, understanding these tools is essential for staying competitive in a technology‑driven industry.

Key Features of Retirement Income Planning Software for Advisors

When evaluating retirement income planning software for advisors, it is crucial to assess whether the platform addresses the full spectrum of client needs. Below are the most sought‑after capabilities that separate leading solutions from the rest.

Comprehensive Cash‑Flow Modeling

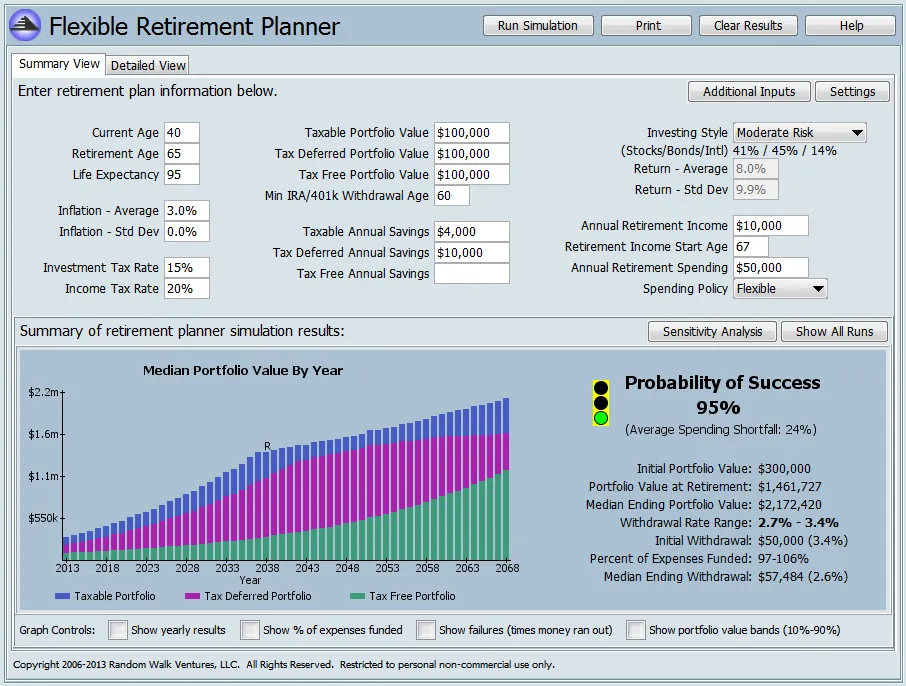

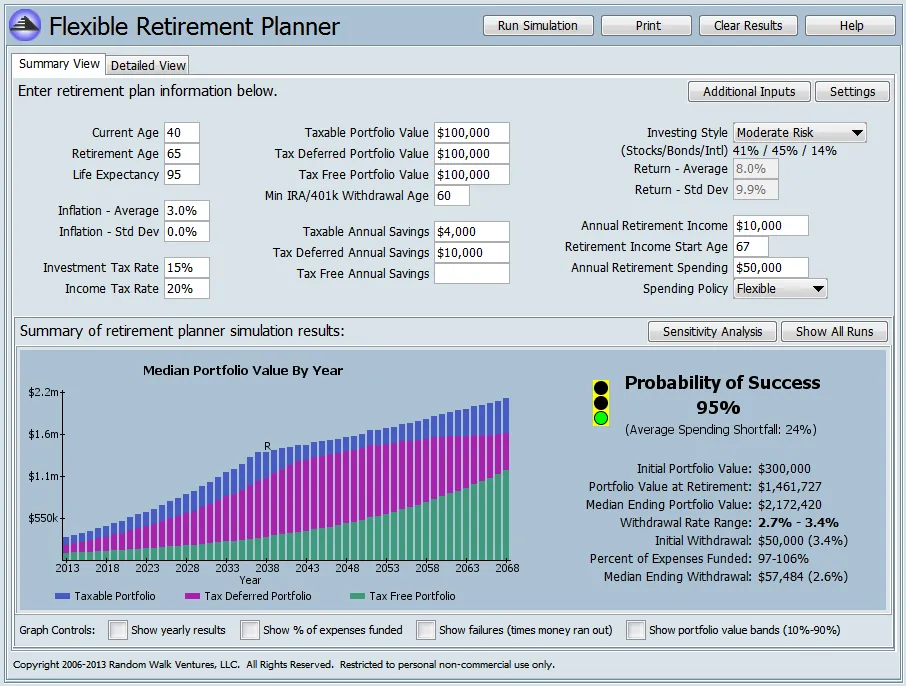

At the heart of any retirement income planning software for advisors lies a robust cash‑flow engine. This feature projects income streams from various sources—pensions, annuities, Social Security, and investment portfolios—over a client’s expected lifespan. The model should allow for scenario analysis, enabling advisors to test the impact of early withdrawals, delayed retirement, or unexpected expenses.

Tax‑Optimized Withdrawal Strategies

Tax efficiency can dramatically affect retirement wealth. The software should automatically recommend withdrawal sequences that minimize taxable income, such as drawing from taxable accounts first, then tax‑deferred accounts, and finally tax‑free sources like Roth IRAs. Integration with clients’ tax brackets and state tax rules ensures the recommendations are truly personalized.

Longevity and Health‑Care Risk Modules

Longevity risk—outliving one’s assets—and health‑care cost inflation are two of the biggest uncertainties retirees face. Advanced retirement income planning software for advisors incorporates actuarial tables and customizable health‑care expense projections, allowing advisors to model the financial impact of long‑term care or unexpected medical bills.

Dynamic Portfolio Rebalancing

Market conditions evolve, and a static allocation can erode a retiree’s income potential. The software should provide dynamic rebalancing alerts based on risk tolerance, drawdown thresholds, and market volatility. Some platforms even suggest tactical adjustments, such as shifting to more conservative assets as clients age.

Client‑Facing Dashboard

Transparency builds trust. A clean, interactive dashboard that clients can access via a secure portal helps them visualize their retirement trajectory, understand the assumptions behind the plan, and explore “what‑if” scenarios on their own. This feature is increasingly expected in modern advisory practices.

Integrating Retirement Income Planning Software for Advisors into Your Practice

Acquiring the right software is only the first step. Seamless integration with existing processes ensures that advisors can deliver value without adding unnecessary complexity.

Data Migration and Connectivity

Most retirement income planning software for advisors offers APIs or direct feeds from custodians, CRM systems, and portfolio management tools. Prior to implementation, map out the data sources—such as account balances, transaction histories, and client demographics—and verify that the software can ingest them automatically. This reduces manual entry errors and saves time.

Training and Certification

Even the most intuitive platform benefits from structured training. Many vendors provide certification programs that cover both the technical aspects of the software and the underlying financial theories. Investing in staff training ensures consistent usage and helps advisors interpret model outputs accurately.

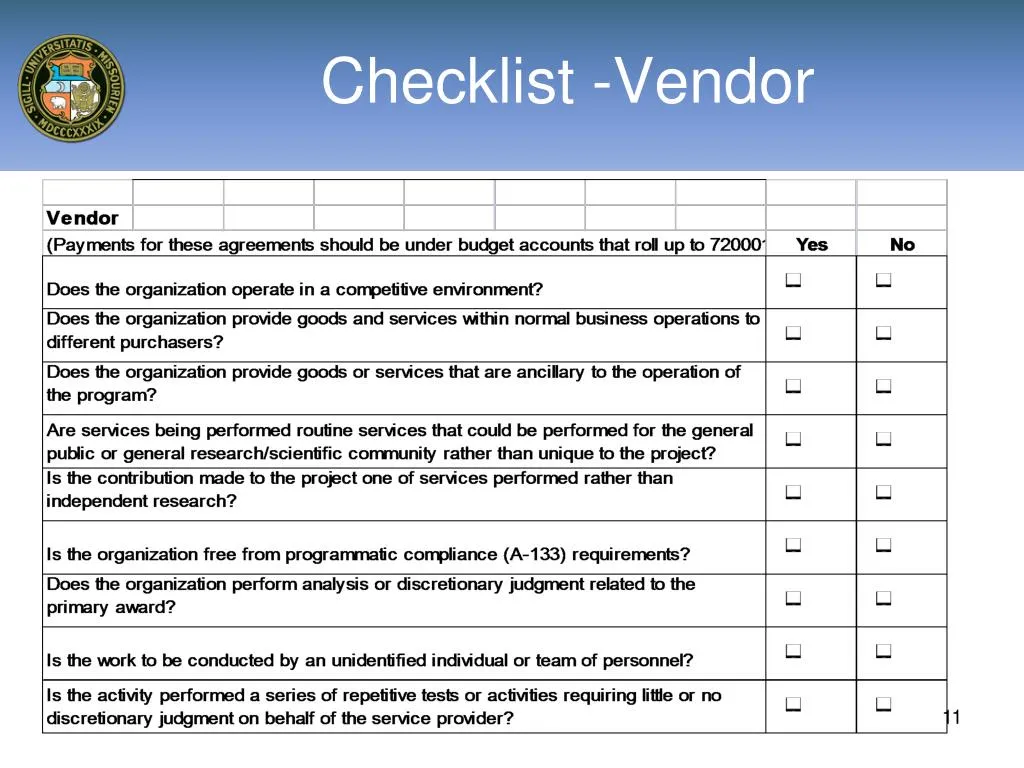

Compliance and Documentation

Regulatory scrutiny around retirement advice is intensifying. Choose a retirement income planning software for advisors that automatically generates compliance‑ready reports, logs assumption changes, and timestamps client interactions. This audit trail protects both the advisor and the firm during examinations.

Pricing Models and ROI Assessment

Software pricing can be subscription‑based, per‑user, or transaction‑based. Conduct a cost‑benefit analysis by estimating the time saved on manual calculations, the potential for higher client retention, and the ability to attract new high‑net‑worth retirees. A well‑chosen platform often pays for itself within the first year through increased efficiency and client satisfaction.

Best Practices for Maximizing Client Outcomes with Retirement Income Planning Software for Advisors

Having a powerful tool is valuable, but the true advantage emerges when advisors apply proven strategies to guide clients toward sustainable retirement income.

Conduct Regular Plan Reviews

Retirement plans should be living documents. Schedule semi‑annual or annual reviews using the software’s scenario analysis capabilities. Adjust assumptions for inflation, market performance, and client life‑events to keep the plan aligned with reality.

Educate Clients on Assumptions

Clients often focus on the final income figure without understanding the underlying assumptions. Use the client‑facing dashboard to walk them through variables like expected return rates, Social Security filing age, and health‑care cost inflation. Informed clients are more likely to adhere to the plan.

Leverage Scenario Planning for Risk Management

Present at least three scenarios—optimistic, base case, and pessimistic—to illustrate how different outcomes affect retirement income. This approach encourages clients to consider contingency funds and insurance products, such as annuities or long‑term care coverage.

Integrate with Broader Financial Planning

Retirement income does not exist in isolation. Ensure the software can export data to comprehensive financial planning platforms, allowing advisors to coordinate estate planning, charitable giving, and legacy goals alongside income strategies.

Utilize Benchmark Comparisons

Many retirement income planning software for advisors include benchmarking tools that compare a client’s projected income against industry standards or peer groups. Highlighting where a client stands can motivate adjustments and reinforce the advisor’s expertise.

Choosing the Right Vendor: A Checklist for Advisors

Selecting a retirement income planning software for advisors involves more than feature comparison; it requires a strategic fit with your firm’s culture, client base, and growth plans. Below is a concise checklist to guide the decision‑making process.

- Scalability: Can the platform handle an expanding client roster without performance degradation?

- Customization: Does it allow you to tailor assumptions, reporting formats, and branding?

- Integration Capability: Are APIs available for seamless data exchange with your existing CRM and portfolio management systems?

- Regulatory Support: Does the software produce compliant documentation and support audit trails?

- Client Experience: Is the client portal intuitive and mobile‑friendly?

- Vendor Support: What level of technical assistance, training, and updates does the provider offer?

By systematically evaluating each criterion, advisors can select a retirement income planning software for advisors that not only meets present needs but also adapts to future industry shifts.

Future Trends Shaping Retirement Income Planning Software for Advisors

The landscape of retirement advice is evolving, and software developers are responding with innovative features that will define the next generation of tools.

Artificial Intelligence and Predictive Analytics

AI-driven engines are beginning to predict market downturns and suggest pre‑emptive asset reallocation. By analyzing vast datasets, these systems can flag potential shortfalls in a client’s income stream before they materialize, giving advisors a proactive advantage.

Integration of Behavioral Finance Insights

Understanding client behavior is essential for retirement success. Emerging platforms embed behavioral finance modules that assess risk aversion, loss aversion, and spending tendencies, allowing advisors to customize communication and recommendation styles.

Real‑Time Data Feeds

Live market data and real‑time account balances enable advisors to run up‑to‑the‑minute cash‑flow simulations. This immediacy is especially valuable during volatile periods when retirement income projections can shift dramatically within days.

Enhanced Security and Privacy Measures

With increasing cyber threats, vendors are adopting zero‑trust architectures, multi‑factor authentication, and end‑to‑end encryption to protect client information. Compliance with standards such as GDPR and CCPA is becoming a baseline requirement.

Putting It All Together: A Practical Example

Consider a 58‑year‑old client, Maria, who has a $1.2 million 401(k), a $350,000 traditional IRA, and a $150,000 Roth IRA. She wishes to retire at 65 and maintain a pre‑retirement income level of 80 % of her current salary. Using a leading retirement income planning software for advisors, her financial planner runs a base‑case scenario that incorporates a 4 % withdrawal rate, delayed Social Security filing until age 70, and a modest 3 % annual portfolio return.

The software projects that Maria can achieve a monthly retirement income of $5,800, but highlights a potential shortfall if inflation exceeds 2.5 % annually. The planner then uses the scenario module to test a higher allocation to dividend‑yielding equities, which improves the projected income to $6,200 while maintaining an acceptable risk profile. The client‑facing dashboard presents these options side‑by‑side, allowing Maria to see the trade‑offs clearly.

After reviewing the analysis, Maria decides to adopt the adjusted portfolio and add a deferred annuity that guarantees $1,200 per month starting at age 70. The planner documents all assumptions, generates a compliance‑ready report, and schedules a semi‑annual review. This workflow illustrates how retirement income planning software for advisors transforms raw data into actionable, client‑centric advice.

Advisors who embrace such technology not only enhance the precision of their recommendations but also free up valuable time to focus on relationship building and strategic counseling.

In an era where retirees are increasingly sophisticated and regulatory demands are tightening, leveraging retirement income planning software for advisors is no longer optional—it is a strategic imperative. By selecting a solution that aligns with firm goals, integrating it thoughtfully, and applying best‑practice methodologies, advisors can deliver resilient, tax‑efficient retirement income plans that stand the test of time.