Table of Contents

- Understanding third party administrators for retirement plan

- Key responsibilities of third party administrators for retirement plan

- Benefits of using third party administrators for retirement plan

- Technology integration and participant experience

- Choosing the right third party administrator for retirement plan

- Evaluation checklist for third party administrators for retirement plan

- Regulatory landscape and the role of third party administrators for retirement plan

- Interaction with auditors and government agencies

- Cost considerations and ROI of third party administrators for retirement plan

- Scalability and future‑proofing

Employers who offer retirement benefits face a complex web of responsibilities. From ensuring that contributions are correctly calculated to filing the required government forms, the administrative load can quickly overwhelm internal staff. Many companies, especially small and mid‑size businesses, turn to specialists who can shoulder these duties while maintaining compliance with ever‑changing regulations. These specialists are known as third party administrators for retirement plan, and they have become an integral part of the modern benefits landscape.

Understanding how third party administrators for retirement plan operate helps business leaders make informed decisions about cost, risk, and employee satisfaction. The partnership is not simply a vendor relationship; it is a strategic alliance that can influence the overall health of a company’s retirement offerings. In the sections that follow, we will walk through the core functions, the advantages of outsourcing, key compliance considerations, and practical tips for selecting the right provider.

Understanding third party administrators for retirement plan

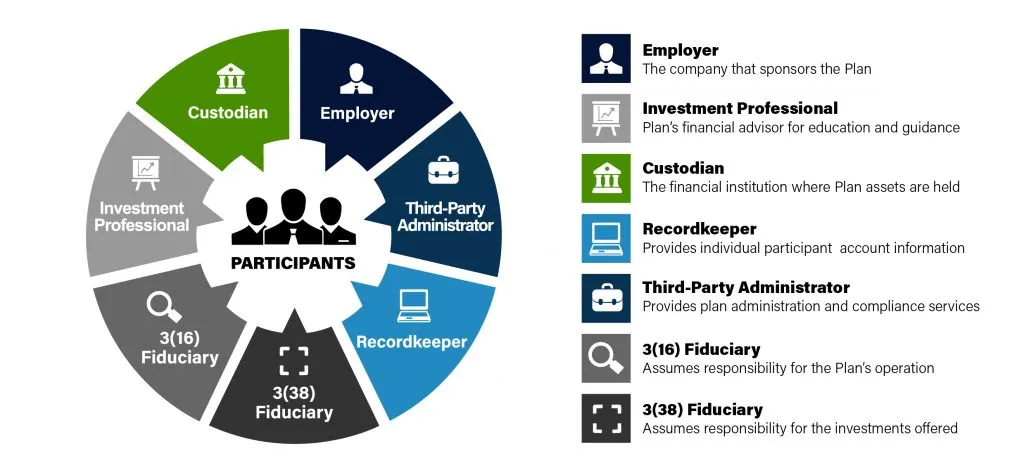

At its core, a third party administrator (TPA) is a service organization that handles the day‑to‑day tasks associated with a retirement plan. While the plan sponsor—the employer—remains the ultimate fiduciary, the TPA performs the operational work that keeps the plan running smoothly. This includes processing participant transactions, preparing and filing Form 5500, conducting nondiscrimination testing, and distributing required notices.

TPAs typically specialize in one or more types of retirement plans, such as 401(k), 403(b), profit‑sharing, or defined benefit arrangements. Their expertise allows them to stay current with the Internal Revenue Service (IRS) and Department of Labor (DOL) regulations, which can be especially valuable for businesses that lack an in‑house compliance team. When a company chooses a third party administrator for retirement plan, it is essentially delegating the technical and administrative burden while retaining strategic control.

Key responsibilities of third party administrators for retirement plan

- Contribution processing: Collecting employee deferrals, employer matches, and profit‑sharing contributions; ensuring accurate allocation to individual accounts.

- Participant services: Managing enrollment, loan requests, hardship withdrawals, and account statements.

- Compliance testing: Performing annual nondiscrimination tests (ADP/ACP, coverage, top‑heavy) to verify that the plan meets IRS rules.

- Reporting and filing: Preparing Form 5500, Schedule D, and other required disclosures; delivering them to the DOL and IRS on time.

- Plan design assistance: Advising sponsors on eligibility, vesting schedules, and contribution formulas that align with business goals.

- Audit support: Supplying documentation and explanations during IRS or DOL examinations.

Because these duties are highly regulated, a TPA must maintain robust internal controls and documentation practices. Errors in contribution calculations or missed filing deadlines can trigger penalties that affect both the sponsor and the participants.

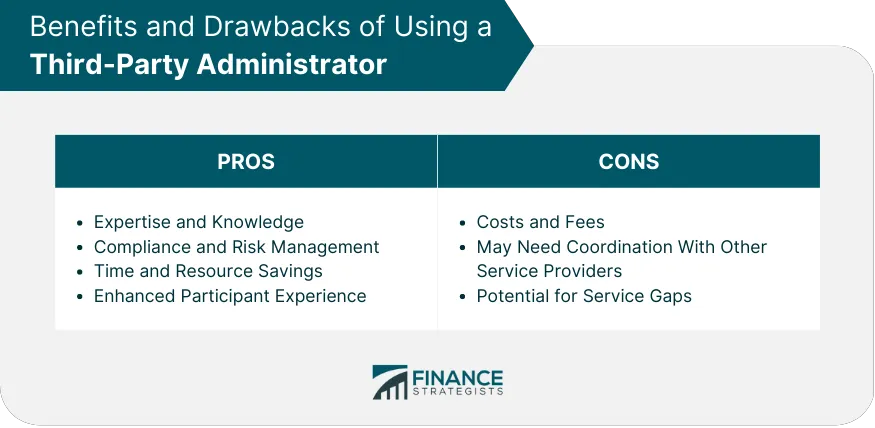

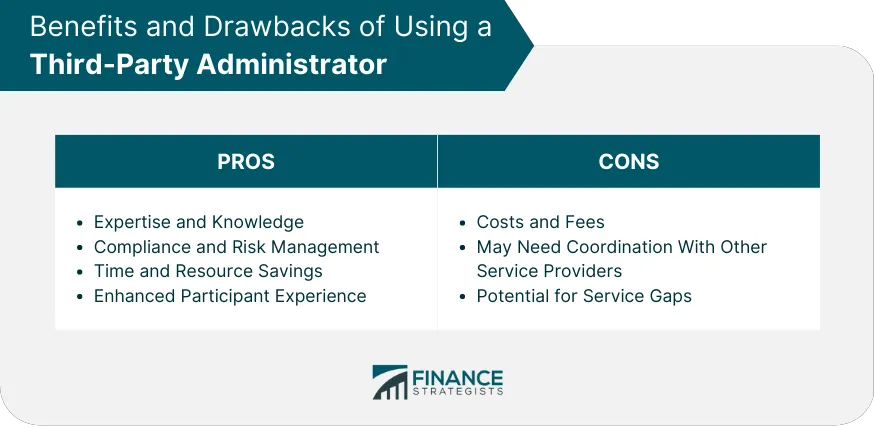

Benefits of using third party administrators for retirement plan

Outsourcing to a qualified TPA offers several tangible advantages. First, it reduces the administrative overhead for internal staff, freeing them to focus on core business activities. Second, TPAs bring specialized knowledge that can improve plan compliance and reduce the risk of costly penalties. Third, many TPAs provide technology platforms that give participants real‑time access to their accounts, investment options, and educational resources.

For small businesses, the cost savings can be significant. A study by the Plan Sponsor Council of America found that companies using third party administrators for retirement plan often experience lower total administration expenses compared to those handling everything internally. Moreover, the professional handling of compliance testing can help the plan avoid “excess contributions” issues that the IRS might otherwise flag—an area explored in depth in the article Can the IRS Take Your Retirement Money? A Detailed Look.

Technology integration and participant experience

Modern TPAs typically offer online portals that integrate payroll data, investment management, and participant communication. These platforms simplify tasks such as updating contribution percentages, selecting investment funds, and viewing balance statements. When the portal is user‑friendly, employee engagement rises, and retirement savings rates improve. In addition, many TPAs support mobile applications, enabling participants to monitor their accounts on the go.

Technology also aids compliance. Automated data feeds reduce manual entry errors, while built‑in validation checks flag potential issues before they become regulatory violations. The combination of streamlined operations and enhanced participant experience makes third party administrators for retirement plan a compelling option for forward‑looking employers.

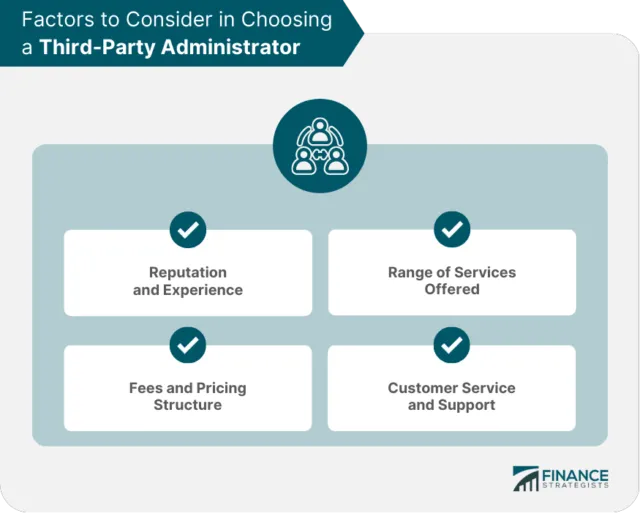

Choosing the right third party administrator for retirement plan

Selecting a TPA is not a one‑size‑fits‑all decision. Employers should evaluate potential providers against a set of criteria that reflects both their current needs and future growth plans. Below are practical steps to guide the selection process.

Evaluation checklist for third party administrators for retirement plan

- Experience and specialization: Verify the provider’s track record with plans of similar size and type.

- Fee structure: Understand whether fees are flat‑rate, per‑participant, or transaction‑based, and compare total cost of ownership.

- Service level agreements (SLAs): Look for clear commitments on response times, filing deadlines, and issue resolution.

- Technology platform: Assess usability, integration capabilities with payroll systems, and data security measures.

- Regulatory expertise: Confirm that the TPA stays current with IRS, DOL, and ERISA updates.

- References and reputation: Speak with existing clients and review third‑party audits or industry awards.

Many employers start their search by reviewing industry reports and directories. It can also be helpful to consult resources that discuss specific plan types, such as the Retirement Plans for Small Businesses Vanguard Guide, which outlines common challenges and best‑practice solutions for smaller sponsors.

Regulatory landscape and the role of third party administrators for retirement plan

The retirement‑plan environment is governed by a layered set of rules: the Employee Retirement Income Security Act (ERISA) sets fiduciary standards, the IRS defines tax qualifications, and the DOL oversees reporting and disclosure. Non‑compliance can lead to disqualification of the plan’s tax‑advantaged status, excise penalties, and even lawsuits.

Third party administrators for retirement plan act as a compliance buffer. They monitor changes such as the SECURE Act, which altered required minimum distributions and catch‑up contribution limits. By keeping the plan sponsor informed and handling the required filings, the TPA minimizes the risk of inadvertent violations. Additionally, many TPAs provide annual compliance reviews and can prepare corrective action plans if a testing failure occurs.

Interaction with auditors and government agencies

During an IRS or DOL audit, the TPA typically serves as the primary point of contact, providing documentation of contributions, participant communications, and testing results. Their familiarity with audit procedures can shorten the examination timeline and reduce the likelihood of adverse findings. In some cases, the TPA may also help the sponsor develop a remediation strategy that restores compliance without excessive penalties.

Cost considerations and ROI of third party administrators for retirement plan

While outsourcing introduces an expense, the return on investment can be measured in several ways. Direct cost savings stem from reduced internal labor hours and avoidance of penalties. Indirect benefits include higher employee participation rates, which improve talent acquisition and retention. Moreover, the expertise provided by a TPA can lead to better plan design choices—such as optimal matching formulas—that enhance overall retirement outcomes for participants.

Employers should evaluate the total cost of ownership, including setup fees, ongoing administration charges, and any ancillary services such as investment consulting. A transparent fee schedule enables sponsors to compare providers on an apples‑to‑apples basis and align expenses with the expected value delivered.

Scalability and future‑proofing

As a business grows, its retirement plan may need to accommodate more participants, additional plan features, or new regulatory requirements. A competent TPA should offer scalable solutions that can be expanded without disruptive system overhauls. This forward‑thinking approach ensures that the partnership remains productive over the long term, rather than requiring a costly switch to another provider down the line.

In summary, third party administrators for retirement plan serve as essential partners for employers seeking to deliver high‑quality retirement benefits while navigating a complex regulatory environment. By handling contributions, compliance testing, reporting, and participant services, TPAs free internal resources and provide expertise that can protect against costly errors. The decision to outsource should be guided by a thorough assessment of experience, technology, fees, and service levels, with an eye toward scalability and future regulatory changes.

When the right TPA is in place, employers can focus on their core mission, confident that the retirement plan operates efficiently, remains compliant, and delivers value to employees. This strategic alignment not only strengthens the organization’s benefits portfolio but also supports the long‑term financial well‑being of its workforce.