Table of Contents

- fisher investments 7 retirement income strategies: Overview of the Framework

- fisher investments 7 retirement income strategies: Core Equity Allocation

- fisher investments 7 retirement income strategies: Dividend‑Focused Holdings

- fisher investments 7 retirement income strategies: Fixed‑Income Ladder

- fisher investments 7 retirement income strategies: Real Estate Exposure

- fisher investments 7 retirement income strategies: Tax‑Managed Withdrawal Plan

- fisher investments 7 retirement income strategies: Inflation‑Protection Mechanism

- fisher investments 7 retirement income strategies: Periodic Portfolio Review & Rebalancing

- Practical Steps to Implement the 7‑Strategy Model

- Potential Pitfalls and How to Avoid Them

- Measuring Success: Key Metrics to Track

Planning for a stable income after leaving the workforce is a challenge that many investors face. Fisher Investments, a global money‑management firm, has distilled its extensive research into a concise framework known as the fisher investments 7 retirement income strategies. This framework is designed to blend safety, growth, and flexibility, helping retirees turn their savings into a dependable cash flow.

The seven‑strategy approach does not rely on a single product or a one‑size‑fits‑all solution. Instead, it weaves together diversified assets, tax‑efficient withdrawals, and disciplined rebalancing. By understanding each component, investors can craft a personalized plan that aligns with their risk tolerance, life expectancy, and legacy goals.

In the sections that follow, we will unpack each of the seven strategies, illustrate how they interact, and provide practical steps for implementation. Whether you are approaching retirement or already drawing down your portfolio, the insights presented here can help you achieve a smoother income journey.

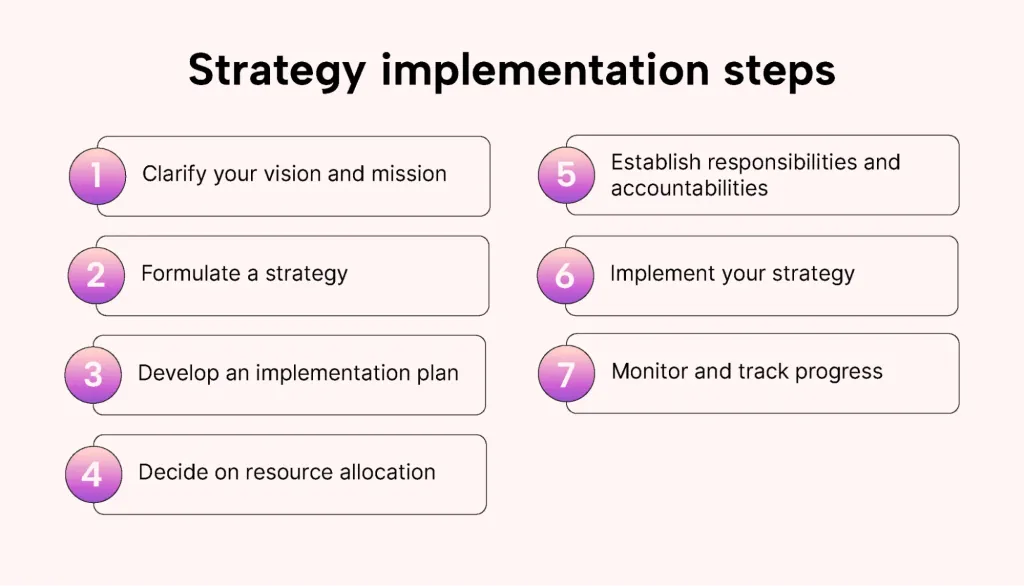

fisher investments 7 retirement income strategies: Overview of the Framework

The core premise of the fisher investments 7 retirement income strategies is to create multiple streams of income that can adapt to market fluctuations. The framework consists of:

- Core Equity Allocation

- Dividend‑Focused Holdings

- Fixed‑Income Ladder

- Real Estate Exposure

- Tax‑Managed Withdrawal Plan

- Inflation‑Protection Mechanism

- Periodic Portfolio Review & Rebalancing

Each pillar serves a distinct purpose, yet together they form a cohesive system that balances growth potential with the need for regular cash flow.

fisher investments 7 retirement income strategies: Core Equity Allocation

At the heart of the approach is a diversified core equity allocation. This component targets long‑term capital appreciation, which is essential for offsetting inflation and extending the life of a retirement portfolio. Fisher Investments typically recommends a blend of large‑cap, mid‑cap, and international stocks, weighted according to the investor’s age and risk profile.

For example, a 65‑year‑old retiree might hold 40 % of the portfolio in equities, while a younger retiree could allocate up to 60 %. The key is to maintain exposure to market upside while avoiding concentration risk. The firm’s research suggests that a well‑managed equity portion can generate an average annual return of 5‑7 % over a 30‑year horizon.

fisher investments 7 retirement income strategies: Dividend‑Focused Holdings

Dividends provide a direct source of cash that can be used for everyday expenses. The strategy emphasizes high‑quality companies with a history of stable or growing dividend payouts. By selecting firms with low payout ratios and strong cash flow, retirees can enjoy reliable income while still allowing the underlying equity to appreciate.

Integrating dividend‑focused holdings reduces the need to sell assets during market downturns, preserving principal for future growth. In practice, a typical allocation might range from 15 % to 25 % of the total portfolio, depending on the retiree’s cash‑flow needs.

fisher investments 7 retirement income strategies: Fixed‑Income Ladder

The fixed‑income ladder is a series of bonds or bond funds with staggered maturities. As each bond reaches maturity, its principal is reinvested into a new, longer‑term bond, creating a rolling stream of predictable cash. This structure helps smooth out interest‑rate risk and provides a baseline income that is largely insulated from equity market volatility.

Fisher Investments often recommends a mix of government, municipal, and high‑quality corporate bonds, with an overall duration that matches the retiree’s time horizon. A 10‑year ladder, for instance, might include bonds maturing every year from year 1 to year 10.

fisher investments 7 retirement income strategies: Real Estate Exposure

Real estate offers two distinct benefits: potential rental income and an inflation hedge. The strategy can be implemented through direct property ownership, real‑estate investment trusts (REITs), or real‑estate‑focused mutual funds. By allocating 10 % to 20 % of assets to real estate, retirees can diversify away from traditional stocks and bonds while capturing income from lease payments.

Because real‑estate values often rise with inflation, this component also supports the inflation‑protection mechanism built into the overall plan.

fisher investments 7 retirement income strategies: Tax‑Managed Withdrawal Plan

Taxes can erode retirement income if not managed carefully. Fisher Investments advocates a tax‑efficient withdrawal sequence that prioritizes taxable accounts first, then tax‑deferred accounts (such as traditional IRAs), and finally tax‑free accounts (like Roth IRAs). This ordering minimizes the tax impact on each dollar withdrawn.

In addition, the strategy recommends using capital‑loss harvesting and strategic Roth conversions during low‑income years to further reduce tax liability. A well‑executed tax plan can increase net income by several percentage points over the course of retirement.

fisher investments 7 retirement income strategies: Inflation‑Protection Mechanism

Inflation erodes purchasing power, making it crucial to include assets that adjust with price increases. Beyond real estate, the framework incorporates Treasury Inflation‑Protected Securities (TIPS) and commodities exposure. By allocating a modest portion—typically 5 % to 10 %—to these instruments, retirees safeguard a portion of their income against rising costs.

Moreover, dividend‑focused holdings and equities historically outpace inflation over long periods, providing an additional buffer.

fisher investments 7 retirement income strategies: Periodic Portfolio Review & Rebalancing

Markets are dynamic; a static allocation will drift over time. Fisher Investments stresses the importance of semi‑annual or annual reviews to assess whether each of the seven pillars still aligns with the retiree’s objectives. Rebalancing involves shifting assets from over‑performing categories back to under‑weighted ones, thereby maintaining the intended risk‑return profile.

Technology tools and robo‑advisors can automate much of this process, but a human oversight layer ensures that life‑event changes—such as health costs or legacy wishes—are incorporated into the plan.

Practical Steps to Implement the 7‑Strategy Model

Turning the theory of the fisher investments 7 retirement income strategies into a functional plan involves a series of concrete actions. Below is a step‑by‑step guide that retirees can follow or discuss with a financial advisor.

- Assess Your Current Situation: Gather statements for all retirement accounts, calculate net worth, and estimate annual expenses.

- Determine Your Risk Tolerance: Use questionnaires or consult a professional to gauge how much market volatility you can comfortably endure.

- Set Target Allocations for Each Pillar: Based on age, income needs, and risk tolerance, decide on the percentage for equities, dividends, bonds, real estate, inflation‑hedge, and cash.

- Select Appropriate Vehicles: Choose mutual funds, ETFs, individual securities, or managed accounts that match each pillar’s objectives. The Fisher Investments retirement guide offers detailed product recommendations.

- Implement a Tax‑Efficient Withdrawal Schedule: Map out which accounts will be drawn from each year, incorporating the tax‑managed withdrawal plan.

- Build a Fixed‑Income Ladder: Purchase bonds or bond funds with staggered maturities, ensuring a steady cash flow.

- Schedule Regular Reviews: Set calendar reminders for semi‑annual portfolio assessments, adjusting allocations as needed.

For small‑business owners, integrating retirement income strategies with company‑sponsored plans can enhance the overall picture. The Retirement Plans for Small Businesses Vanguard Guide provides complementary insights on how employer‑sponsored accounts fit within the broader retirement income framework.

Potential Pitfalls and How to Avoid Them

Even a robust model like the fisher investments 7 retirement income strategies can falter if certain common mistakes are made. Below are the most frequent traps and practical mitigation tactics.

- Over‑Concentration in One Pillar: Relying too heavily on dividends or real estate can expose the retiree to sector‑specific risks. Maintain the diversified mix prescribed by the seven‑strategy model.

- Neglecting Inflation: Ignoring the inflation‑protection component can erode purchasing power. Regularly revisit the TIPS and commodity allocations.

- Improper Tax Sequencing: Withdrawing from tax‑free accounts first can lead to higher taxable income later. Follow the tax‑managed withdrawal hierarchy.

- Failure to Rebalance: Letting allocations drift can shift the portfolio into a higher‑risk profile than intended. Use automated rebalancing tools or schedule manual checks.

- Insufficient Liquidity: Holding too much in illiquid assets, such as certain real‑estate investments, may force a sale at an inopportune time. Keep a cash buffer equal to at least six months of expenses.

Measuring Success: Key Metrics to Track

To determine whether the fisher investments 7 retirement income strategies are delivering the expected outcomes, retirees should monitor a set of quantitative and qualitative indicators.

| Metric | What It Indicates |

|---|---|

| Withdrawal Rate | Percentage of portfolio taken out each year; aim for 3‑4 % to sustain longevity. |

| Real Return | Portfolio return after accounting for inflation; should exceed the inflation rate. |

| Tax Efficiency Ratio | Net income after taxes divided by gross withdrawals; higher is better. |

| Asset Allocation Drift | Difference between target vs. actual percentages; triggers rebalancing. |

| Liquidity Ratio | Cash and cash equivalents divided by annual expenses; a ratio >1 is desirable. |

Regularly reviewing these metrics helps retirees stay aligned with their financial goals and make timely adjustments.

In summary, the fisher investments 7 retirement income strategies present a comprehensive, multi‑layered roadmap for turning accumulated wealth into a sustainable, inflation‑adjusted income stream. By blending core equity growth, dividend cash flow, fixed‑income stability, real‑estate diversification, tax‑smart withdrawals, inflation protection, and disciplined rebalancing, the model addresses the most common challenges faced by retirees.

Implementing this framework requires careful planning, periodic monitoring, and a willingness to adapt as personal circumstances evolve. Yet, for those who follow the structured approach, the payoff is a retirement experience marked by financial confidence and the freedom to enjoy the years ahead.