Table of Contents

- Simple Retirement Plans for Small Businesses: Core Options Explained

- Why Simple Retirement Plans for Small Businesses Matter

- Step‑by‑Step Guide to Implementing a Simple Retirement Plan

- 1. Assess Your Business Needs and Employee Demographics

- 2. Choose the Right Plan Structure

- 3. Select a Trusted Financial Institution

- 4. Draft a Clear Plan Document

- 5. Communicate the Plan to Employees

- 6. Set Up Payroll Integration

- 7. Maintain Ongoing Compliance

- Cost Considerations and Budgeting Tips

- Leverage Group Purchasing Power

- Encourage Employee Self‑Direction

- Utilize Tax Deductions

- Common Pitfalls and How to Avoid Them

- Neglecting Eligibility Rules

- Underestimating Employee Education

- Missing Filing Deadlines

- Real‑World Example: A Boutique Marketing Agency’s Journey

- Future‑Proofing Your Retirement Offering

Running a small business often means juggling many priorities—cash flow, customer satisfaction, and growth strategies—all while trying to attract and retain quality employees. One powerful tool that can tip the scales in a company’s favor is a well‑designed retirement offering. While large corporations have the resources to create complex, multi‑tiered plans, small employers can achieve comparable results with simple retirement plans for small businesses. These plans are cost‑effective, easy to administer, and can still deliver meaningful retirement savings for staff.

In this article we walk through the most common types of retirement solutions, outline the steps needed to set them up, and highlight practical tips that keep administration straightforward. By the end, business owners will have a clear roadmap to launch a retirement program that meets regulatory requirements and boosts employee morale—without the headaches that often accompany larger, more intricate schemes.

Whether you are a boutique retail shop, a tech startup, or a family‑owned service firm, the principles discussed here apply across industries. The emphasis is on simplicity, transparency, and scalability so that the plan can grow alongside your business.

Simple Retirement Plans for Small Businesses: Core Options Explained

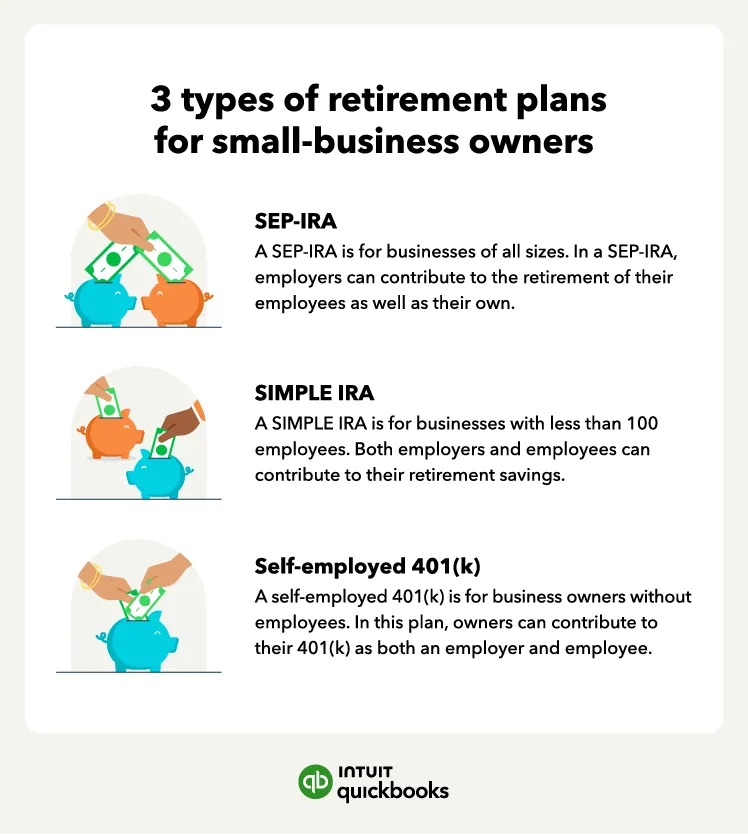

When the phrase simple retirement plans for small businesses appears, most owners think of low‑cost, low‑maintenance solutions. The three most popular choices are:

- SEP IRA (Simplified Employee Pension) – Ideal for businesses that want to make contributions on behalf of employees without requiring employee salary deferrals.

- SIMPLE IRA (Savings Incentive Match Plan for Employees) – Designed for companies with up to 100 employees, offering both employer and employee contributions.

- Payroll‑deducted 401(k) or Safe Harbor 401(k) – Provides the flexibility of a traditional 401(k) while keeping compliance requirements manageable.

Each option balances contribution limits, administrative burden, and eligibility criteria differently. Choosing the right one depends on the size of your workforce, cash‑flow considerations, and the level of employee participation you anticipate.

Why Simple Retirement Plans for Small Businesses Matter

Employees today expect more than just a paycheck; they look for benefits that signal long‑term security. Offering a retirement plan can:

- Improve recruitment and retention, especially among skilled workers who weigh benefits heavily.

- Provide tax advantages for both employer and employee, reducing taxable income while fostering savings.

- Enhance company culture by demonstrating a commitment to employee welfare.

These outcomes align directly with the core goals of simple retirement plans for small businesses: delivering value without overwhelming the owner with paperwork.

Step‑by‑Step Guide to Implementing a Simple Retirement Plan

Implementing a retirement solution is a multi‑phase process, but it can be broken down into manageable steps. Below is a practical roadmap that any small business can follow.

1. Assess Your Business Needs and Employee Demographics

Start by gathering data on employee ages, tenure, and salary levels. This helps determine which plan type maximizes participation. For instance, younger workforces might favor a 401(k) with matching contributions, while older employees may appreciate the higher contribution limits of a SEP IRA.

2. Choose the Right Plan Structure

Match your assessment to one of the core options:

- SEP IRA – Best when you want to contribute only as an employer and keep paperwork minimal.

- SIMPLE IRA – Works well if you want to involve employees with salary deferrals and provide a modest match.

- Payroll‑deducted 401(k) – Suitable when you aim for higher contribution caps and want to offer a Roth option.

All three meet the IRS’s definition of “simple,” but the nuances affect long‑term costs and flexibility.

3. Select a Trusted Financial Institution

Partner with a provider that offers low‑fee custodial services and user‑friendly online portals. Many banks and brokerage firms have dedicated small‑business retirement platforms that handle record‑keeping, compliance testing, and employee education. An example of a reliable source for plan insights is the Fisher Investments Retirement Guide PDF, which outlines best practices for plan selection and ongoing management.

4. Draft a Clear Plan Document

The plan document acts as the legal backbone. Even simple plans require a written agreement that outlines eligibility, contribution formulas, vesting schedules, and distribution rules. Many providers supply a template that can be customized to reflect your business’s specific policies.

5. Communicate the Plan to Employees

Effective communication drives participation. Host an informational session, distribute a concise brochure, and provide an FAQ sheet. Highlight key benefits such as tax deductions, employer matching (if applicable), and the ease of payroll deductions. Including real‑world examples—like how a modest 3% match can double an employee’s savings over ten years—makes the concept tangible.

6. Set Up Payroll Integration

Most payroll software can automatically deduct employee contributions and calculate employer matches. Work closely with your payroll provider to ensure the correct codes are used and that contributions are transferred to the chosen custodian on schedule.

7. Maintain Ongoing Compliance

Even the simplest plans must meet IRS filing deadlines (e.g., Form 5500‑E). Choose a provider that offers annual compliance reviews or consider hiring a third‑party administrator for peace of mind. Regular audits prevent penalties and keep the plan in good standing.

Cost Considerations and Budgeting Tips

One of the biggest concerns for small business owners is cost. While the name “simple” suggests minimal expense, there are still fees to account for:

- Setup fees – Some providers charge a one‑time onboarding fee, typically ranging from $0 to $250.

- Annual administrative fees – These can be a flat rate per participant or a percentage of assets, often between 0.25% and 0.75% of assets under management.

- Investment expense ratios – Choose low‑cost index funds or ETFs to keep expense ratios below 0.10% whenever possible.

To keep costs low, consider the following budgeting strategies:

Leverage Group Purchasing Power

Some financial institutions offer discounted fees for businesses that join a consortium of small employers. This collective bargaining can reduce per‑employee costs dramatically.

Encourage Employee Self‑Direction

Allowing participants to choose their own investment options reduces the need for employer‑managed portfolios, cutting advisory fees. Provide a curated list of low‑cost index funds and let employees select what fits their risk tolerance.

Utilize Tax Deductions

Employer contributions are tax‑deductible, which can offset a portion of the administrative expenses. Keep detailed records to maximize these deductions during tax season.

Common Pitfalls and How to Avoid Them

Even simple plans can run into trouble if certain best practices are ignored. Below are frequent mistakes and practical solutions.

Neglecting Eligibility Rules

Failing to properly define who qualifies for the plan can lead to discrimination claims. Ensure that eligibility criteria (e.g., age, service length) are applied uniformly.

Underestimating Employee Education

Without clear guidance, employees may not enroll or may make poor investment choices. Provide ongoing workshops and digital resources. The AT&T Benefits Center for Retirees offers a model of comprehensive employee education that can be adapted for small firms.

Missing Filing Deadlines

Late filing of Form 5500‑E can result in penalties. Set calendar reminders well before the due date and consider automating the filing process through your plan provider.

Real‑World Example: A Boutique Marketing Agency’s Journey

To illustrate how the concepts translate into practice, let’s follow the story of “Creative Pulse,” a marketing agency with 12 employees. The owner, Maya, wanted to improve retention after a key designer left for a competitor offering a 401(k).

Maya evaluated three options and settled on a SIMPLE IRA because it allowed employee contributions and required only a modest 3% matching contribution. She partnered with a local credit union that offered zero setup fees and a flat $30 annual fee per participant.

After a brief onboarding session, the agency rolled out the plan via its existing payroll software. Within six months, 75% of staff had enrolled, and the average contribution rate was 4% of salary. The tax deduction from employer matching saved Maya’s business $2,400 in the first year, effectively covering the administrative costs.

This case shows that even a small firm can reap tangible benefits by selecting a plan that aligns with its size, culture, and financial capacity.

Future‑Proofing Your Retirement Offering

As your business expands, the retirement plan you start with should be flexible enough to evolve. Here are three ways to future‑proof your choice:

- Scalable Architecture – Choose a provider that supports upgrades, such as moving from a SIMPLE IRA to a full‑service 401(k) without migrating data.

- Employee Feedback Loops – Conduct annual surveys to gauge satisfaction and adjust plan features (e.g., adding Roth options) based on demand.

- Regulatory Monitoring – Stay informed about legislative changes, like the SECURE Act, that could affect contribution limits or eligibility.

By maintaining an adaptable framework, you ensure that the retirement solution remains relevant and valuable as both the workforce and regulations shift.

In summary, implementing simple retirement plans for small businesses is a strategic move that blends affordability with employee empowerment. By following the step‑by‑step guide, keeping an eye on costs, and avoiding common pitfalls, owners can deliver a retirement benefit that strengthens their competitive edge while fostering long‑term financial security for their teams. The journey begins with a clear assessment, a thoughtful plan choice, and a commitment to transparent communication—simple steps that yield lasting impact.