Table of Contents

- Retirement Planning for High‑Net‑Worth Individuals: Core Pillars

- Wealth Preservation Through Diversified Asset Allocation

- Tax Efficiency: Minimizing the Bite of Federal and State Obligations

- Generating Reliable Income Without Eroding Principal

- Legacy Creation and Philanthropy

- Risk Management: Protecting Assets from Market, Legal, and Personal Threats

- Choosing the Right Advisory Team

- Questions to Vet Potential Advisors

- Implementing a Technology‑Enabled Retirement Strategy

- Leveraging Digital Platforms for Ongoing Review

- Case Study: A Hypothetical High‑Net‑Worth Retirement Journey

- Monitoring and Adjusting the Plan Over Time

- When to Re‑Balance or Re‑Allocate

When wealth accumulates beyond the ordinary, the conversation about the future shifts from “how much will I have?” to “how can I preserve, grow, and pass on what I’ve built?” For high‑net‑worth individuals, retirement is less about a simple paycheck and more about orchestrating a suite of sophisticated strategies that address tax exposure, legacy goals, and lifestyle flexibility. This article walks through the essential components of retirement planning for high‑net‑worth individuals, weaving together practical steps, common pitfalls, and the latest tools that can make the journey smoother.

The first step is acknowledging that traditional retirement frameworks—relying on Social Security, a 401(k), or a modest personal savings plan—often fall short for those whose assets span multiple classes, including private equity, real estate, and alternative investments. A nuanced plan must incorporate the unique risk profile, liquidity needs, and philanthropic ambitions that typically accompany substantial wealth. Below, each major pillar is broken down, providing a roadmap that can be customized to fit any high‑net‑worth portfolio.

In the sections that follow, you’ll find actionable guidance on everything from selecting the right fiduciary to structuring charitable giving, and even leveraging digital assets safely. By the end, the goal is for you to feel equipped to design a retirement strategy that not only protects your wealth but also aligns with the legacy you wish to leave.

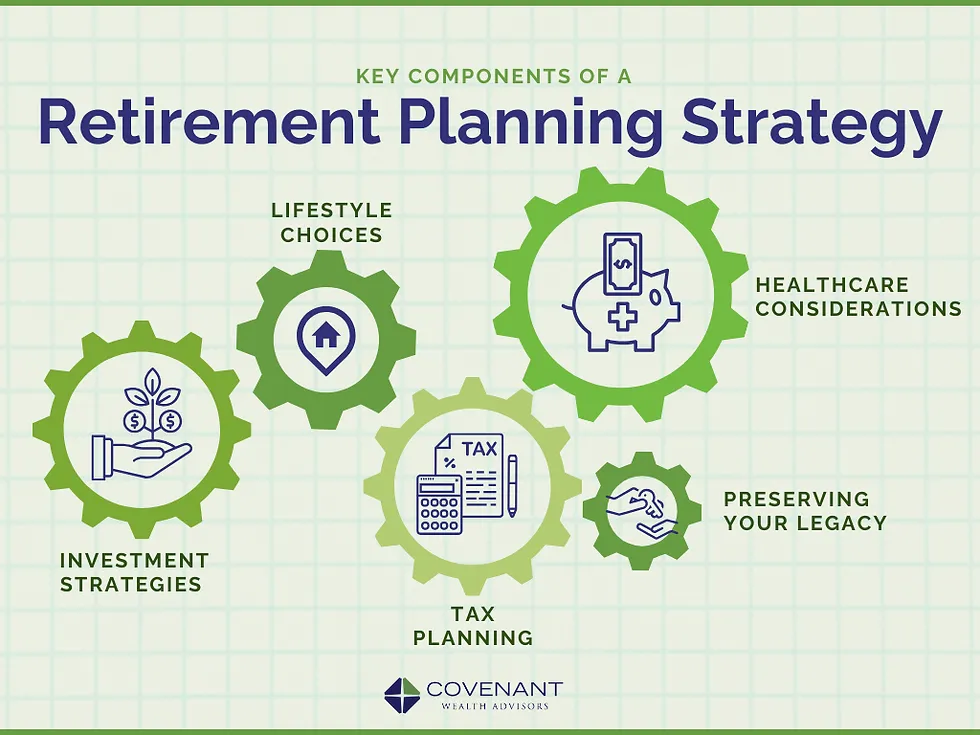

Retirement Planning for High‑Net‑Worth Individuals: Core Pillars

Effective retirement planning for high‑net‑worth individuals rests on five interlocking pillars: wealth preservation, tax efficiency, income generation, legacy creation, and risk management. Each pillar requires a tailored approach that reflects the complexity of a sizable portfolio.

Wealth Preservation Through Diversified Asset Allocation

A diversified portfolio is the foundation of any long‑term plan, but for high‑net‑worth investors the definition of diversification expands beyond stocks and bonds. Consider adding:

- Direct real‑estate holdings that generate steady cash flow and offer inflation hedging.

- Private equity or venture capital stakes, which can provide outsized returns when managed prudently.

- Alternative assets such as hedge funds, commodities, and even carefully vetted digital currencies.

These assets often have lower correlation with public markets, reducing overall portfolio volatility. However, they also bring liquidity challenges. A prudent strategy includes a “liquidity buffer”—typically 10‑15% of total net worth—in highly liquid instruments (e.g., short‑term Treasury bills, money‑market funds) to meet unexpected expenses without forcing the sale of illiquid holdings at inopportune times.

Tax Efficiency: Minimizing the Bite of Federal and State Obligations

Tax considerations dominate retirement planning for high‑net‑worth individuals. The goal is to structure income and capital gains in the most tax‑advantaged way possible. Key tactics include:

- Maximizing tax‑deferred accounts such as defined‑benefit plans or cash‑balance pensions that allow large contributions beyond the limits of a typical 401(k).

- Utilizing charitable remainder trusts (CRTs) to receive an immediate charitable deduction while retaining an income stream for life.

- Strategic asset location—placing tax‑inefficient assets (e.g., REITs, high‑yield bonds) inside tax‑advantaged accounts and holding tax‑efficient assets (e.g., equities) in taxable accounts.

For those holding digital assets, the step‑by‑step guide on withdrawing money from Crypto.com offers practical insights on converting crypto to fiat while managing capital gains exposure.

Generating Reliable Income Without Eroding Principal

Unlike the average retiree who may depend on a single source of income, high‑net‑worth individuals can blend multiple streams:

- Qualified dividend income from blue‑chip equities taxed at favorable rates.

- Rental cash flow from carefully selected properties with long‑term leases.

- Systematic withdrawal plans from private equity or venture funds that provide periodic distributions.

One sophisticated method is the “bucket strategy,” which divides assets into three buckets: short‑term cash for immediate needs, medium‑term income‑generating assets, and long‑term growth investments. This approach helps maintain spending power while preserving growth potential.

Legacy Creation and Philanthropy

Many high‑net‑worth individuals view retirement as an opportunity to shape a lasting impact. Integrating philanthropy early can yield both emotional satisfaction and tax benefits. Options include:

- Donor‑advised funds (DAFs) that allow donors to contribute now, receive an immediate tax deduction, and recommend grants over time.

- Family foundations that provide a structured vehicle for multi‑generational charitable giving.

- Estate planning tools such as generation‑skipping trusts to transfer wealth efficiently across multiple generations.

When constructing a legacy plan, coordinate closely with an estate attorney and a tax advisor to align the charitable components with overall wealth transfer objectives.

Risk Management: Protecting Assets from Market, Legal, and Personal Threats

Risk management for high‑net‑worth retirees is multi‑faceted:

- Insurance coverage—including umbrella policies, long‑term care insurance, and, where appropriate, captive insurance structures.

- Legal safeguards—using entities such as limited liability companies (LLCs) or limited partnerships (LPs) to isolate assets.

- Cybersecurity measures—particularly crucial for those holding digital assets; employing hardware wallets, multi‑factor authentication, and regular security audits.

A well‑designed risk framework not only preserves wealth but also provides peace of mind, enabling retirees to focus on the experiences they value most.

Choosing the Right Advisory Team

Retirement planning for high‑net‑worth individuals is too complex for a single professional. A collaborative team typically includes a wealth manager, tax attorney, estate planner, and, when relevant, a specialist in alternative assets. Look for advisors who hold fiduciary status, as this legal duty requires them to act in your best interest.

Questions to Vet Potential Advisors

- What is your experience with clients whose net worth exceeds $10 million?

- Can you provide case studies that illustrate successful tax‑efficient retirement structures?

- How do you coordinate with my existing legal and accounting professionals?

Transparency around fees is equally important. Many high‑net‑worth advisors work on a percentage‑of‑assets model, but a hybrid approach—combining a base fee with performance incentives—can align interests more closely.

Implementing a Technology‑Enabled Retirement Strategy

Modern technology offers powerful tools for monitoring and adjusting a retirement plan in real time. Portfolio management platforms can consolidate data from traditional brokerage accounts, private equity dashboards, and even crypto wallets, providing a single view of net worth. Automation features, such as scheduled rebalancing and tax‑loss harvesting, help maintain the plan’s efficiency without constant manual intervention.

Leveraging Digital Platforms for Ongoing Review

Adopting a secure, cloud‑based solution enables you to share information instantly with your advisory team, reducing the risk of miscommunication. When evaluating platforms, prioritize those that comply with stringent security standards (e.g., SOC 2, ISO 27001) and offer granular permission settings for each stakeholder.

For a deeper dive into how technology can streamline your retirement plan, see the detailed guide to retirement planning for high net worth individuals, which outlines specific software solutions and integration best practices.

Case Study: A Hypothetical High‑Net‑Worth Retirement Journey

Consider a 58‑year‑old entrepreneur with a net worth of $25 million, comprised of a 30% stake in a tech startup, $5 million in rental properties, $3 million in a diversified public‑equity portfolio, and $2 million in crypto assets. The individual’s goals include:

- Maintaining a lifestyle that requires $500,000 per year.

- Leaving a charitable legacy of at least $5 million.

- Ensuring that the tech‑startup equity can be liquidated over a 10‑year horizon without triggering a market crash.

Applying the pillars discussed:

- Liquidity Buffer: The advisor creates a $3 million cash reserve in short‑term Treasury instruments.

- Tax‑Efficient Income: Rental properties generate $250,000 of net cash flow, while qualified dividends from the public‑equity portfolio add another $150,000.

- Crypto Management: Using the Crypto.com withdrawal guide, the client converts $500,000 of crypto into a taxable account, timing sales to stay within the lower capital‑gain brackets.

- Charitable Planning: A CRT is established, providing a $2 million charitable deduction now and an income stream of $120,000 per year for life.

- Risk Controls: The tech‑startup stake is transferred into a family limited partnership, limiting personal liability and facilitating a gradual buy‑out plan.

Over the next decade, the plan delivers consistent income, preserves capital, and fulfills the client’s philanthropic ambition, illustrating how a disciplined, multi‑faceted approach to retirement planning for high‑net‑worth individuals can produce both financial security and meaningful impact.

Monitoring and Adjusting the Plan Over Time

Retirement is not a static phase; market conditions, tax law, and personal circumstances evolve. An annual review—often conducted with the full advisory team—is essential. Key metrics to track include:

- Asset allocation drift relative to the target percentages.

- Effective tax rate on realized gains and income.

- Liquidity ratios to ensure cash needs are met without distress sales.

- Progress toward charitable and legacy goals.

During the review, consider incorporating new investment opportunities, such as a T. Rowe Price Retirement 2060 Fund, which can serve as a diversified, low‑maintenance growth component for the long‑term bucket. An overview of the T. Rowe Price Retirement 2060 Fund provides insight into its risk‑adjusted performance and suitability for high‑net‑worth portfolios.

When to Re‑Balance or Re‑Allocate

Significant market moves—like a sharp rise in interest rates or a tech‑sector correction—may warrant a tactical shift. However, avoid over‑reacting to short‑term volatility; instead, focus on whether the underlying assumptions of the retirement plan remain valid. If not, a strategic re‑allocation, perhaps moving some private‑equity exposure to more liquid assets, may be prudent.

By maintaining a disciplined review cadence and leveraging technology for real‑time data, high‑net‑worth retirees can stay ahead of risks and capitalize on emerging opportunities.

Retirement planning for high‑net‑worth individuals is a sophisticated undertaking that blends financial acumen, legal expertise, and personal values. When approached methodically—through diversified preservation, tax‑smart structures, reliable income streams, purposeful legacy design, and robust risk management—wealth can continue to serve both the retiree’s lifestyle and the broader impact they wish to make. The journey requires collaboration, continual learning, and the willingness to adjust as life unfolds, but the payoff is a retirement that feels both secure and meaningful.