Table of Contents

- Retirement Planning for High Net Worth Individuals: An Overview

- Key Considerations in Retirement Planning for High Net Worth Individuals

- Investment Strategies for Affluent Retirees

- Diversified Portfolios Tailored to Lifestyle

- Alternative Assets as Income Sources

- Estate and Legacy Planning

- Trust Structures and Charitable Giving

- Income Generation and Cash Flow Management

- Withdrawal Strategies That Preserve Wealth

- Building a Professional Advisory Team

- Choosing the Right Advisors

Reaching the stage where a comfortable retirement is within reach is a milestone most people cherish. For high net worth individuals, the journey involves a distinct set of challenges and opportunities that require a sophisticated, multidimensional approach. The goal is not merely to preserve wealth, but to ensure it continues to grow, supports a desired lifestyle, and can be transferred according to personal wishes.

Because the financial landscape for affluent retirees is often more complex—featuring multiple asset classes, substantial tax considerations, and legacy ambitions—each decision must be made with both short‑term liquidity needs and long‑term family objectives in mind. This article walks through the essential components of retirement planning for high net worth individuals, offering a roadmap that integrates investment strategy, tax efficiency, estate preservation, and the role of trusted advisors.

Retirement Planning for High Net Worth Individuals: An Overview

At its core, retirement planning for high net worth individuals revolves around three pillars: preserving capital, generating reliable income, and facilitating an orderly transfer of assets. Unlike a typical 401(k) scenario, affluent retirees often hold diversified portfolios that include public equities, private equity, real estate, and sometimes even collectibles. Each asset type reacts differently to market cycles, tax law changes, and inflation pressures.

Moreover, the tax environment becomes a decisive factor. Capital gains, qualified dividends, and ordinary income are taxed at varying rates, and the interaction between these rates and an individual’s marginal tax bracket can dramatically affect after‑tax returns. Effective retirement planning therefore requires an integrated tax‑aware strategy that aligns with personal risk tolerance and lifestyle goals.

Key Considerations in Retirement Planning for High Net Worth Individuals

- Liquidity Needs: Even with substantial assets, cash flow must be sufficient to cover daily expenses, healthcare, travel, and unexpected costs without forcing the sale of illiquid investments.

- Tax Efficiency: Minimizing exposure to federal, state, and international taxes while complying with regulations is essential for preserving wealth.

- Legacy Objectives: Whether the aim is to leave a charitable legacy, support future generations, or both, estate planning must be woven into the retirement blueprint.

- Risk Management: A balanced approach that protects against market volatility, longevity risk, and potential legal challenges is critical.

These considerations form the foundation for a plan that can adapt to life’s inevitable changes. The next sections dive deeper into each component, providing actionable insights that align with the unique needs of high net worth retirees.

Investment Strategies for Affluent Retirees

When assets exceed the typical retirement savings threshold, the focus shifts from simple growth to a nuanced blend of preservation, income generation, and opportunistic growth. A well‑structured portfolio for high net worth individuals typically blends traditional and alternative investments, each selected for its risk‑adjusted return profile and tax characteristics.

Diversified Portfolios Tailored to Lifestyle

A diversified portfolio is not merely a collection of stocks and bonds; it often includes private equity, venture capital, real estate investment trusts (REITs), and even hedge funds. The allocation should reflect the retiree’s risk tolerance, desired income stream, and the need for capital appreciation. For instance, a 60/40 split between equities and fixed income might be appropriate for a moderate risk profile, while a higher allocation to alternative assets could better meet income goals and provide inflation protection.

Many high net worth retirees also incorporate low‑volatility equity strategies, such as those offered by the T. Rowe Price Retirement 2060 Fund – Comprehensive Overview, which blends growth‑oriented equities with a glide path designed to reduce risk as the investor ages.

Alternative Assets as Income Sources

Real estate remains a cornerstone for many wealthy retirees, offering both cash flow and potential appreciation. Direct ownership, syndications, and REITs each present distinct liquidity and management implications. In addition, investments in private credit or structured products can deliver higher yields while maintaining a level of principal protection.

When evaluating alternatives, it is vital to assess the underlying cash‑flow characteristics, correlation to traditional markets, and tax treatment. For example, qualified dividends from dividend‑focused ETFs are often taxed at a lower rate than ordinary income, making them attractive for income‑seeking retirees.

Estate and Legacy Planning

Wealth preservation is incomplete without a solid estate plan that respects the retiree’s values and mitigates estate tax exposure. For high net worth individuals, the estate planning process typically involves a suite of legal instruments—trusts, charitable vehicles, and family limited partnerships—each crafted to achieve specific goals.

Trust Structures and Charitable Giving

Irrevocable trusts, such as irrevocable life insurance trusts (ILITs) or charitable remainder trusts (CRTs), can remove assets from the taxable estate while providing income streams to beneficiaries or charitable causes. A well‑designed CRT, for instance, allows the retiree to receive a fixed income for life, with the remainder passing to a chosen charity, thereby reducing estate taxes and supporting philanthropic goals.

Integrating charitable giving into the retirement plan also offers a dual benefit of fulfilling personal legacy desires and unlocking tax deductions. The Is Merrill Lynch Good for Retirement? An In‑Depth Look article explores how certain financial institutions structure charitable giving programs to align with high net worth clients’ objectives.

Income Generation and Cash Flow Management

Generating a reliable, tax‑efficient income stream is perhaps the most visible aspect of retirement planning for high net worth individuals. The goal is to meet lifestyle expenses while preserving the underlying capital for future generations.

Withdrawal Strategies That Preserve Wealth

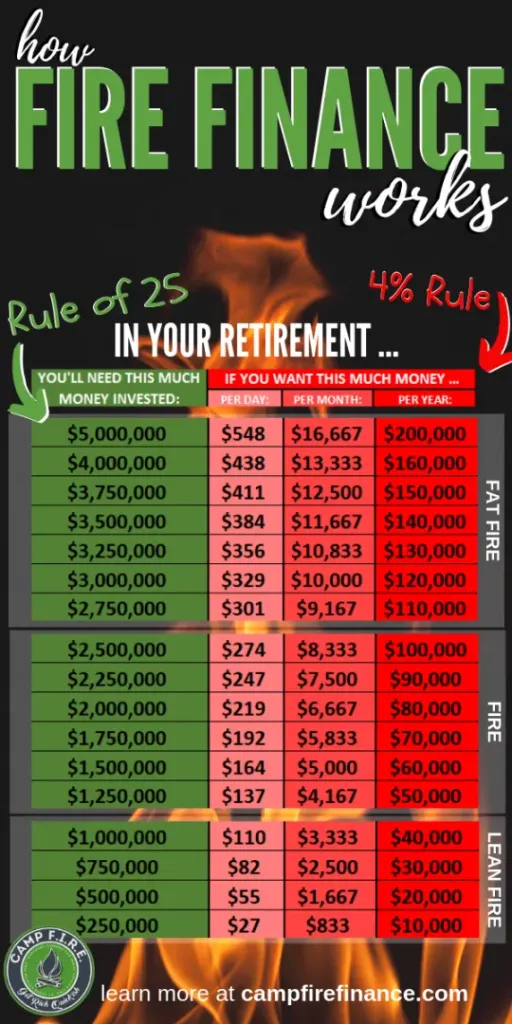

Traditional withdrawal rules—such as the 4% rule—are often too simplistic for complex portfolios. A more refined approach considers the tax impact of each withdrawal, the sequencing of asset sales, and the use of tax‑advantaged accounts. For example, drawing first from taxable accounts with high‑cost basis can minimize capital gains taxes, while postponing Social Security or pension benefits may increase their eventual value.

In addition, retirees may employ systematic withdrawal plans that allocate a fixed percentage of the portfolio each year, adjusted for inflation. This method helps maintain a consistent standard of living while allowing the remaining assets to continue growing.

Building a Professional Advisory Team

No single individual can master the myriad facets of retirement planning for high net worth individuals. A collaborative team of experts—including a wealth manager, tax attorney, estate planner, and fiduciary accountant—ensures that each piece of the puzzle fits seamlessly.

Choosing the Right Advisors

The selection process begins with evaluating the advisor’s fiduciary status, fee structure, and experience with high net worth clients. Transparent fee arrangements—whether flat‑fee, retainer, or asset‑based—help align the advisor’s interests with those of the client. Moreover, advisors should demonstrate a track record of integrating investment strategy with tax and estate planning, rather than treating each discipline in isolation.

For retirees interested in a holistic view, the Retirement Planning for High Networth Individuals – A Comprehensive Guide offers a deep dive into building a coordinated advisory network that can adapt to evolving circumstances.

In practice, regular reviews—quarterly or semi‑annually—allow the team to adjust the plan for market shifts, legislative changes, or personal milestones such as the birth of a grandchild or the sale of a major asset. This proactive stance keeps the retirement plan resilient and aligned with long‑term objectives.

Ultimately, retirement planning for high net worth individuals is a living document. It evolves as markets fluctuate, tax laws are revised, and family dynamics shift. By focusing on liquidity, tax efficiency, diversified investments, and a robust advisory network, affluent retirees can enjoy a comfortable, purposeful retirement while ensuring that their legacy endures for generations to come.